Rethinking the Glide Path: What Research Tells Us About Social Security and Your Retirement Portfolio

A summary of academic findings — and what they mean for the conversations worth having with your advisor.

Among the most consequential decisions a retiree faces, few receive the careful attention they deserve. How a portfolio balances stocks and bonds over time — and how that balance coordinates with guaranteed income sources such as Social Security — can be the difference between a retirement that sustains itself comfortably and one that comes up short when it matters most.

A 2024 study published in the <em>Journal of Financial Planning</em> examined these questions with rigorous depth, exploring how guaranteed income, risk tolerance, bequest objectives, and asset allocation strategies interact across thousands of simulated retirement scenarios. The findings are, in several respects, counterintuitive — and for that reason, they deserve the attention of anyone who is planning for or already living in retirement.

“One of the biggest threats to a portfolio’s success at providing lifetime income is a big loss in value early, rather than later, in retirement.”

Waggle and Agrrawal, June 2024

A glide path describes how a portfolio’s allocation between stocks and bonds is designed to evolve over time. The conventional approach — reflected in most target-date retirement funds — calls for holding a higher proportion of equities during working years, then gradually shifting toward bonds as retirement approaches and progresses. The rationale is grounded in sound logic: bonds offer more stability, and a retiree who experiences a significant market loss does not have the time or future income to recover from it.

The researchers examined five distinct glide path strategies, each representing a different trajectory for equity allocation across a 30-year retirement horizon:

- Decreasing Fast</strong> — equity allocation falls by 40% over 30 years

- Decreasing Slow</strong> — equity allocation falls by 20% over 30 years

- Constant</strong> — equity allocation is rebalanced to its starting level each year

- Slow</strong> — equity allocation rises by 20% over 30 years

- Increasing Fast</strong> — equity allocation rises by 40% over 30 years

Starting equity allocations from 0% to 100% were tested across each glide path — a total of 43 unique portfolio strategies — and each was evaluated across 1,000 Monte Carlo simulations using long-term return and inflation assumptions for large-cap equities and 10-year Treasury bonds.

The Role of Social Security

The study’s most practically significant finding centers on Social Security — and on the cost of ignoring it. Many portfolio analyses treat the investable portfolio in isolation, as though guaranteed income streams do not exist. The researchers found that this approach leads to meaningfully different, and often suboptimal, portfolio recommendations.

For retirees with moderate or high risk aversion, factoring Social Security into the analysis typically points toward a higher initial equity allocation than an analysis that excludes it would suggest. At first glance, this may seem to work against conventional wisdom. But the underlying logic is sound: guaranteed income functions as a floor. When a meaningful portion of living expenses is covered regardless of market conditions, the investable portfolio can take on more measured risk in pursuit of long-term growth — particularly for those with goals around legacy and wealth transfer.

The study expressed wealth in terms of the ratio of investable assets to the present value of Social Security, examining scenarios in which Social Security represented 75%, 33%, and 17% of overall wealth. As Social Security’s proportional share increased, the case for higher initial equity allocations in the remaining portfolio strengthened accordingly.

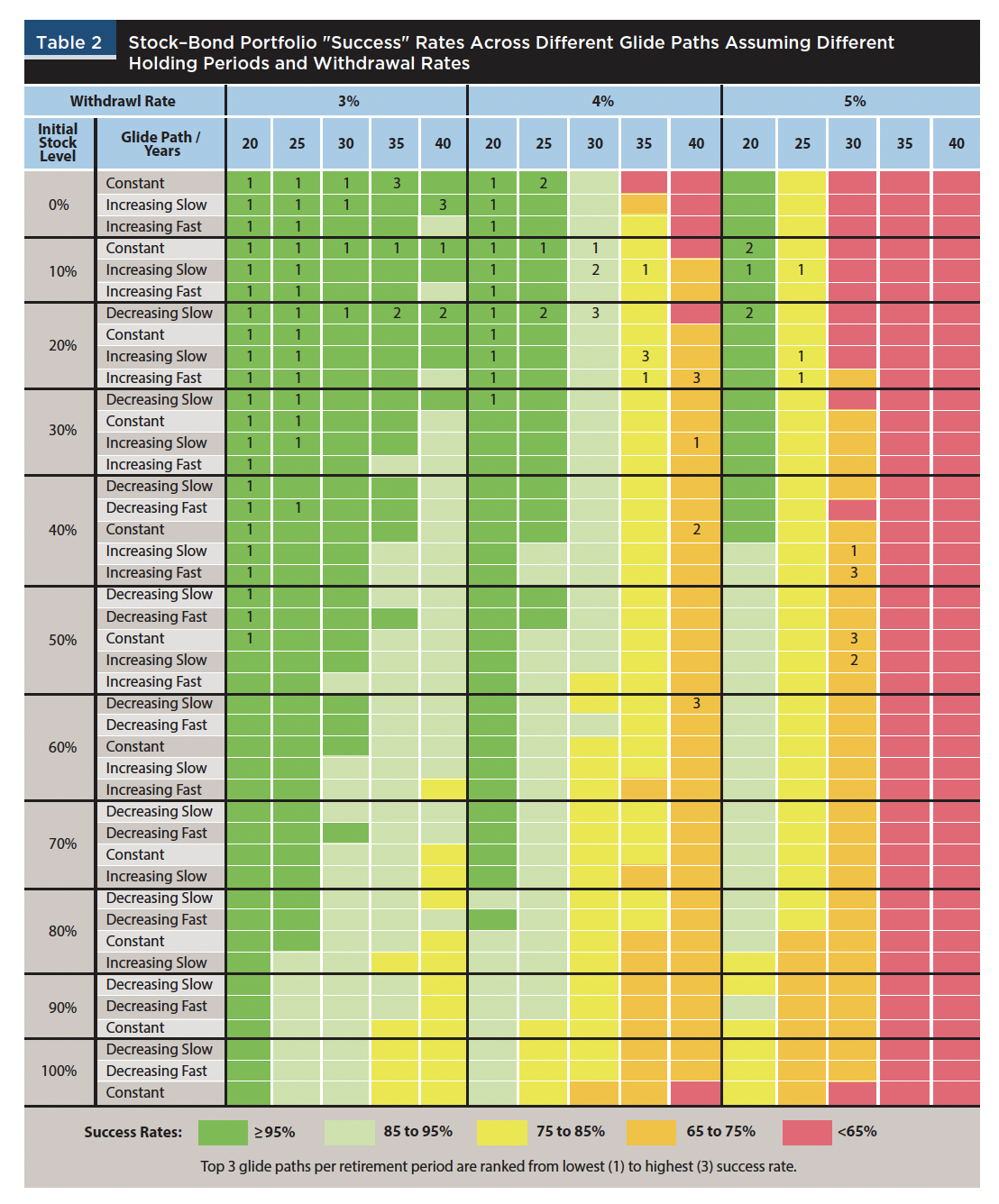

Portfolio success rates

The first lens through which the research evaluated these strategies was straightforward: could a given portfolio sustain inflation-adjusted withdrawals for the full retirement period without being exhausted? Three withdrawal rates were examined — 3%, 4%, and 5% of initial portfolio value — across retirement horizons ranging from 20 to 40 years.

The results illustrate a familiar tension. At a 3% withdrawal rate, a wide range of glide paths succeeded across most time horizons, providing planners and clients with meaningful flexibility. At 4%, outcomes began to diverge meaningfully depending on starting equity levels and glide path direction. At 5%, the picture becomes considerably more challenging, particularly for retirement horizons extending 35 to 40 years — where even the best-performing strategies fell well short of certainty.

The tables below are reproduced directly from the original research. The top three performing glide paths for each scenario are ranked 1 through 3

Table 2 — Portfolio Success Rates

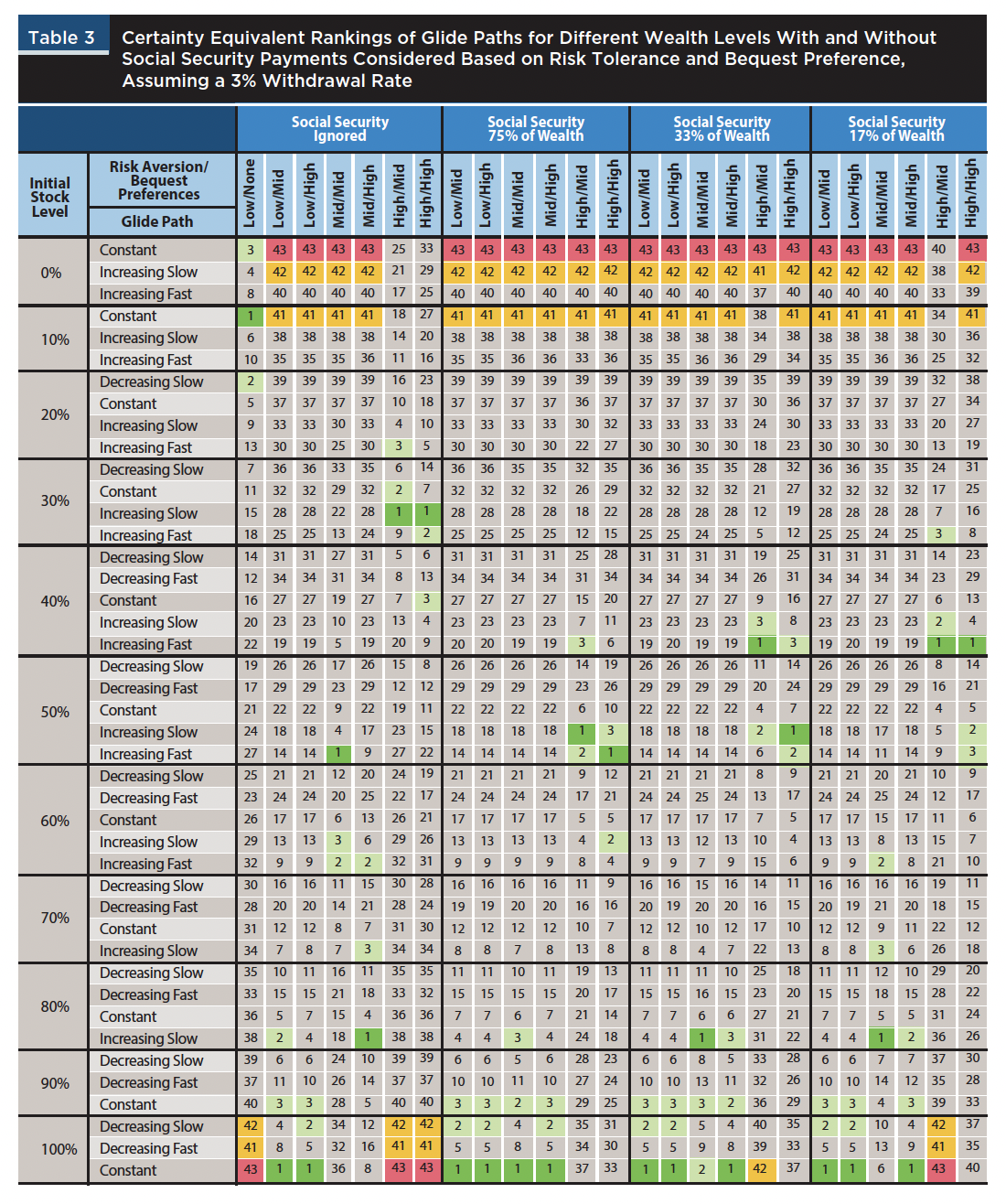

Table 3 — Portfolio Success Rates: 3% Withdrawal Rate

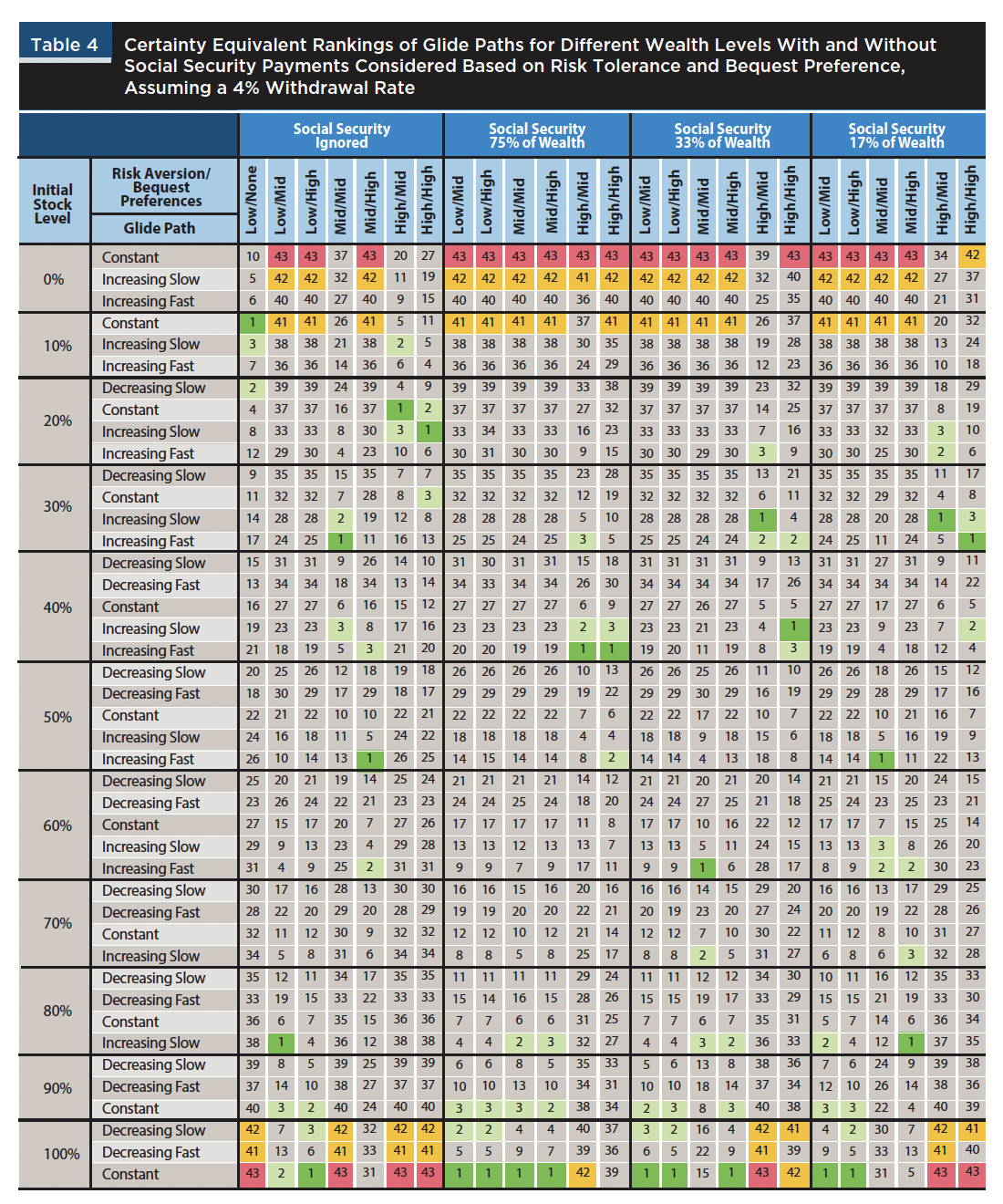

Table 4 — Portfolio Success Rates: 4% Withdrawal Rate

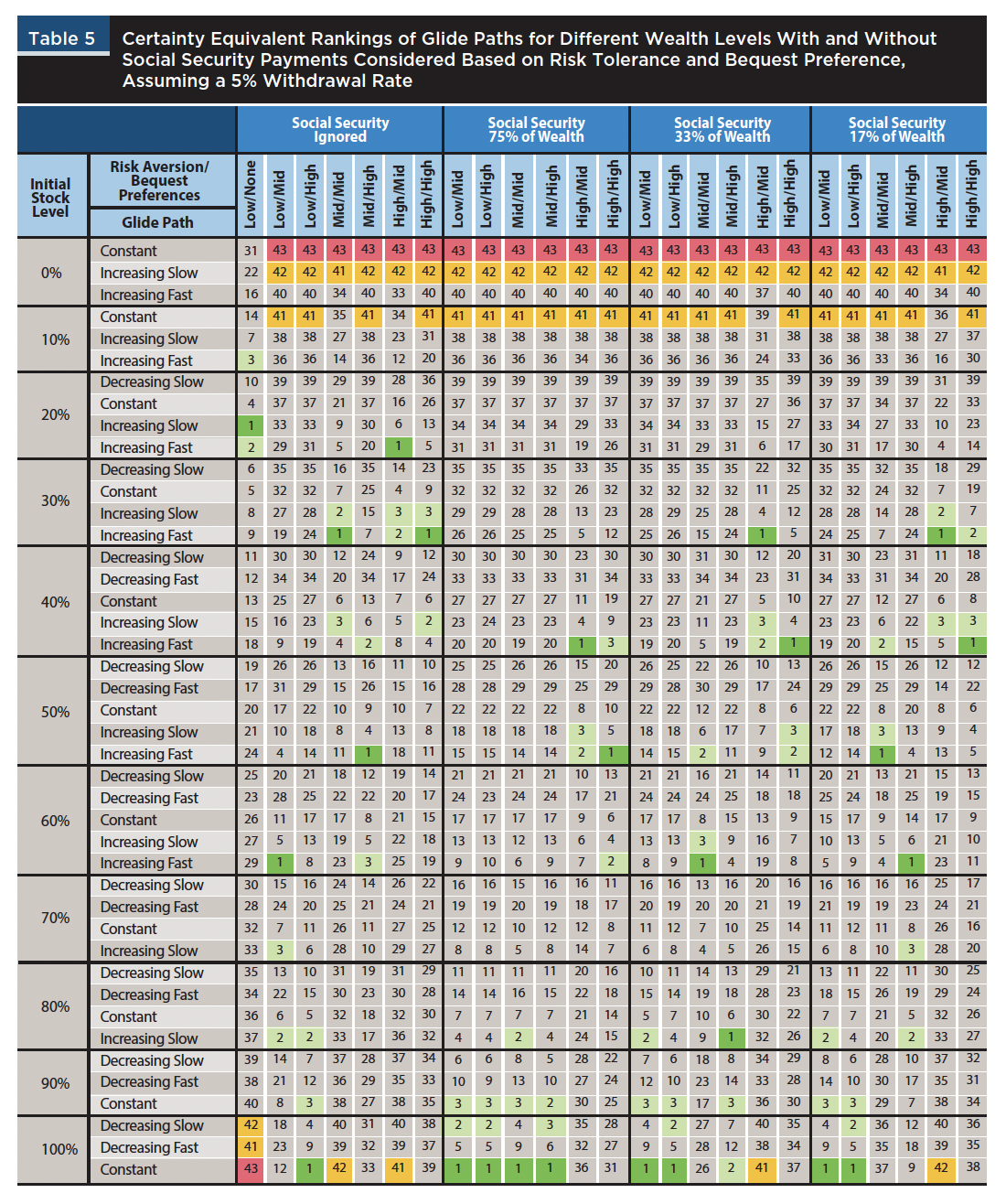

Table 5 — Portfolio Success Rates: 5% Withdrawal Rate

Beyond success rates: the utility framework

A binary success-or-failure measure, while useful, has inherent limitations. A portfolio that provides income for 30 years and leaves one dollar in the account is technically “successful” — yet it tells a fundamentally different story than one that sustains withdrawals and leaves a meaningful inheritance for heirs. Likewise, for a retiree whose Social Security covers the majority of living expenses, a portfolio shortfall carries far less consequence than for someone whose portfolio bears the full weight of retirement income.

To capture this complexity, the researchers applied a constant relative risk aversion (CRRA) utility framework that evaluates outcomes across three dimensions simultaneously: the percentage of desired income actually received each year, the retiree’s level of risk aversion, and the strength of their preference for leaving a financial legacy. The result is a ranking of all 43 glide path strategies from most to least optimal — not merely by survival, but by the quality of the retirement experience as the individual retiree would realistically value it.

Key findings and their implications

Several conclusions from this research stand apart as especially relevant for clients approaching or navigating retirement.First, ignoring Social Security distorts the analysis. When the research compared optimal portfolios with and without Social Security factored in, the recommended strategies diverged substantially — particularly for retirees with moderate or high risk aversion. In some cases, the optimal starting equity allocation shifted by 20 to 30 percentage points depending on whether guaranteed income was included. Financial plans that treat the investable portfolio in isolation are, by definition, working with an incomplete picture.

Second, rising glide paths merit serious consideration. Conventional guidance directs retirees to reduce equity exposure over time. The research found that for a broad range of investor profiles — especially those with bequest goals — increasing equity allocations throughout retirement frequently produced superior utility outcomes. The logic is intuitive once examined: beginning with a more conservative allocation reduces vulnerability to the sequence-of-returns risk that most threatens early retirees, while the gradual increase in equity exposure supports long-term growth as the portfolio establishes its footing.

Third, the optimal path is deeply personal. Risk aversion, bequest preferences, withdrawal rates, and the size of Social Security relative to total wealth all interact to produce different optimal outcomes. There is no universal answer — only an answer that is right for a given individual, in a given set of circumstances, with a given set of goals.

What this means for you

Retirement planning, at its best, is an act of precision. The research summarized here affirms what we at Cestia have long believed: the decisions that shape retirement outcomes should be engineered around the full reality of your financial life — your income sources, your risk profile, your time horizon, and what you want your wealth to accomplish for the people and causes you care about.

Social Security is a genuine and material asset. Its guaranteed, inflation-adjusted income stream fundamentally changes the construction of an optimal retirement portfolio. A rising glide path, starting conservatively and building equity exposure as the portfolio matures through the critical early retirement years, may deliver meaningfully better outcomes for many retirees — not despite their caution, but because of it.

References

Doug Waggle, Ph.D., and Pankaj Agrrawal, Ph.D. (2024). Guaranteed Income and Optimal Retirement Glide Paths.Journal of Financial Planning, 37(6), 74–94,

Disclosures

- Cestia Wealth Management is not a legal tax professional. We offer tax gap analysis for clients who desire to have a comprehensive financial plan, which requires in-depth tax strategy and planning as a distinct part of the overall customized solution. Please consult your tax professional on all matters addressed in this report.

- Wealth Mechanics™ is a registered trademark of Cestia Wealth Management. Unauthorized use of the trademark, including but not limited to commercial use, reproduction, or imitation without explicit written permission from Cestia Wealth Management, is strictly prohibited.

- Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance is no guarantee of future results. Please note that individual situations can vary. Therefore, the information presented here should only be relied upon when coordinated with individual professional advice.

- Citations to Internal Revenue Code sections, Treasury regulations, IRS notices and revenue procedures, and Tax Court decisions reflect guidance and case law in effect as of the date of publication and are subject to change.

- Advisory services offered through NewEdge Advisors, LLC, a registered investment adviser. Securities offered through NewEdge Securities, LLC. Member FINRA/SIPC. NewEdge Advisors, LLC and NewEdge Securities, LLC are wholly owned subsidiaries of NewEdge Capital Group, LLC.

- This material was prepared with the assistance of AI. All content has been reviewed, edited, and approved by Cestia Wealth Management prior to use.