Order from Chaos: What a Nail Board Can Teach Diligent Investors About Markets

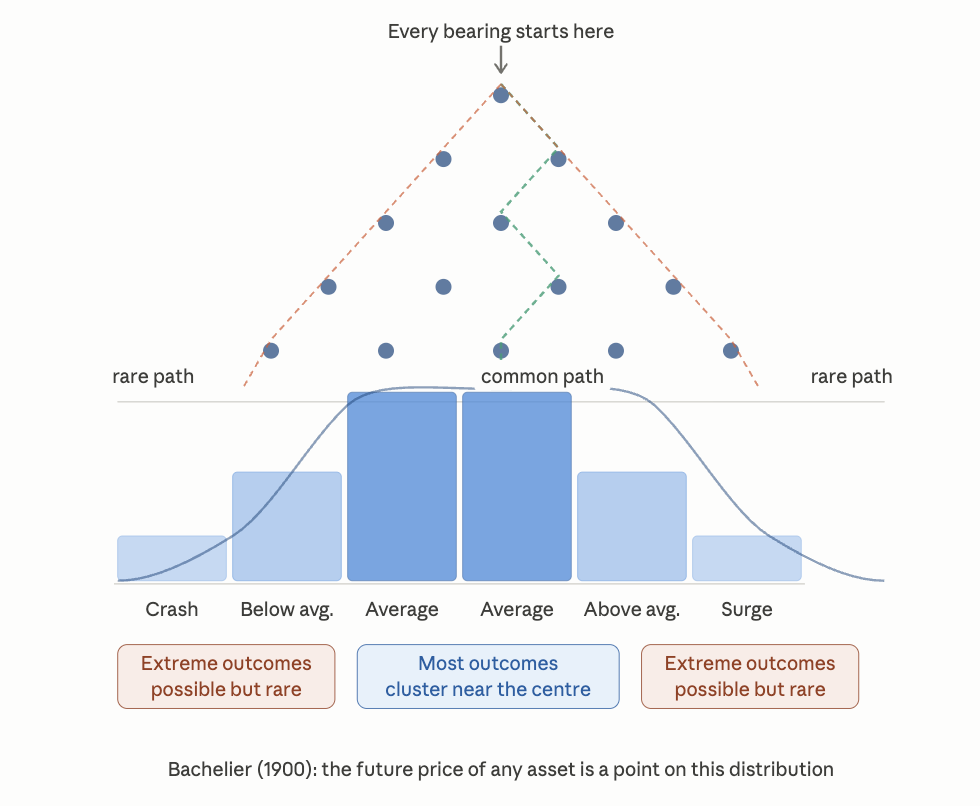

There is a device, deceptively simple in its construction, that has fascinated mathematicians and scientists for over a century. The Galton board — named after the Victorian polymath Sir Francis Galton — is little more than a triangular array of pegs mounted above a row of collection bins. Steel bearings are dropped from the top one by one, each striking the first peg and deflecting left or right in what appears to be a perfectly random choice. The bearing falls to the next row, bounces again, and again, all the way to the bottom.

Watch a thousand bearings fall and something remarkable appears. No single bearing follows a predictable path. Yet the collection of all of them — those thousands of individual random journeys — assembles itself into a smooth, symmetrical bell curve. The centre bins are always full. The edge bins are always nearly empty. Chaos, repeated at sufficient scale, produces order.

This is not a trick. It is mathematics, and it has meaningful implications for anyone committed to building wealth with intention and consistency.

Why the middle wins

The logic of the Galton board is combinatorial. A bearing that ends up in the far-left bin must have deflected left at virtually every single peg it encountered. A bearing in the far-right bin must have gone consistently right. Both outcomes are possible — but both require a long, unbroken streak of the same result. The middle, by contrast, is reachable by an enormous variety of paths: left-right-left-right, right-left-right-left, and countless other combinations all converge there. The centre bins fill not because they are “correct” but because there are simply more routes leading to them.

The probability of extreme outcomes is real. It is also, by the structure of the board itself, geometrically rare.

Louis Bachelier and the random walk of prices

In 1900, a young French mathematician named Louis Bachelier submitted a doctoral thesis that his examiners found elegant but commercially peculiar. Its title was Théorie de la Spéculation, and its central argument was startling for its time: the future price of a financial asset is not knowable. It is governed by a distribution. Bachelier proposed that price movements follow a “random walk” — each step independent of the last, shaped by the continuous arrival of new information that no participant can fully anticipate. He derived the same mathematical structure that underlies the Galton board: the probability of a price being at any given level after some interval follows a normal, bell-shaped distribution centred on the present price. His work predated Einstein’s paper on Brownian motion by five years and laid the foundations for everything that would later become modern financial theory.

The insight was not that markets are irrational. It was that they are so efficient at absorbing information that the residual — the part that actually moves prices — behaves like pure noise. In Bachelier’s model, the expected future price of a stock is simply its present price. All the skill, all the analysis, all the forecasting, combines to define the centre of the distribution. What actually happens is the bearing finding its own path through the pegs.

What this means for the diligent investor

At Cestia, we believe that wealth is a verb, not a noun. It is built ring by ring — each one shaped by adversity, good fortune, conquered challenges, and the decisions made with clear eyes and a long horizon. The Galton board offers a useful lens for understanding why consistency and structure matter more than trying to predict where any single bearing will land.

A few implications follow from this directly.

First, extreme outcomes — the far bins on the board — do happen. They are genuinely rare, but rare is not the same as impossible. Markets crash. They also surge well beyond what fundamentals would justify. An investor who treats the tails of the distribution as purely theoretical is making the same error as an engineer who designs a bridge only for average weather. A panoramic understanding of markets requires acknowledging that the full width of the board is always in play.

Second, because there are so many paths to middling outcomes and so few to extreme ones, the overwhelming majority of short-term price movements will be modest. This is why volatility that feels dramatic in the moment tends to mean-revert over time. Individual bearings are erratic. The pile beneath the board is smooth. Quick gains can be exhilarating — but our clients know that building true wealth requires a consistent, long-term strategy, not a wager on which bin the next bearing will find.

Third, and perhaps most important, adding more independent bearings — more diversified positions — does not change the shape of the distribution. It sharpens it. A portfolio of uncorrelated assets concentrates outcomes more tightly around the centre. The law of large numbers, Galton’s own observation, is among the oldest and most reliable tools available to any investor building rings of wealth with a meticulous focus on the granular details of their financial life.

The paradox of the visible pattern

There is a quiet paradox at the heart of the Galton board. The pattern — the bell curve — is perfectly predictable. The path of any individual bearing is not. Markets offer the same paradox to those who pursue their long-term goals with mindful sensibility. In aggregate, over time, returns cluster around economic fundamentals. In the short run, any individual stock, sector, or index can find itself anywhere in the distribution.

Bachelier understood this over a century ago. The market, he argued, yields no systematic profit to either buyer or seller — not because it is passive or irrational, but because every piece of information that could predict the next move is already embedded in the current price. The peg at the top of the board is always the same. It is everything that happens after the bearing leaves your hand that cannot be controlled.

The Galton board asks investors to make peace with that reality — not with passivity, but with the kind of calm confidence that comes from a well-engineered financial strategy. You choose which board to play on, how many bearings to drop, and how long to wait for the pile to take its shape. Throughout the changes, challenges, and goals that define your financial journey, the distribution remains your most dependable guide.

That is, more or less, what markets have always rewarded.

Sources

On Louis Bachelier and the random walk of prices

Bachelier, L. (1900). Théorie de la Spéculation. Annales Scientifiques de l’École Normale Supérieure, 17, 21–88. Reprinted in: Cootner, P. H. (ed.) (1964). The Random Character of Stock Market Prices. MIT Press.

Davis, M. & Etheridge, A. (2006). Louis Bachelier’s Theory of Speculation: The Origins of Modern Finance. Princeton University Press.

Courtault, J-M. et al. (2000). “Louis Bachelier: On the Centenary of Théorie de la Spéculation.” Mathematical Finance, 10(3), 341–353.

On the Galton board

Galton, F. (1889). Natural Inheritance. Macmillan. pp. 63–70. Facsimile available at galton.org.

Schneider, I. (2001). “The Quincunx: History and Mathematics.” Statistical Papers, 42, 143–169.

On the efficient market hypothesis

Fama, E. F. (1965). “Random Walks in Stock Market Prices.” Financial Analysts Journal, 21, 55–59.

Fama, E. F. (1970). “Efficient Capital Markets: A Review of Theory and Empirical Work.” Journal of Finance, 25, 383–417.

Disclosures

- Cestia Wealth Management is not a legal tax professional. We offer tax gap analysis for clients who desire to have a comprehensive financial plan, which requires in-depth tax strategy and planning as a distinct part of the overall customized solution. Please consult your tax professional on all matters addressed in this report.

- Wealth Mechanics™ is a registered trademark of Cestia Wealth Management. Unauthorized use of the trademark, including but not limited to commercial use, reproduction, or imitation without explicit written permission from Cestia Wealth Management, is strictly prohibited.

- Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance is no guarantee of future results. Please note that individual situations can vary. Therefore, the information presented here should only be relied upon when coordinated with individual professional advice.

- Citations to Internal Revenue Code sections, Treasury regulations, IRS notices and revenue procedures, and Tax Court decisions reflect guidance and case law in effect as of the date of publication and are subject to change.

- Advisory services offered through NewEdge Advisors, LLC, a registered investment adviser. Securities offered through NewEdge Securities, LLC. Member FINRA/SIPC. NewEdge Advisors, LLC and NewEdge Securities, LLC are wholly owned subsidiaries of NewEdge Capital Group, LLC.

- This material was prepared with the assistance of AI. All content has been reviewed, edited, and approved by Cestia Wealth Management prior to use.